Matthew Henderson

Associate Director, Residential Research

Associate Director, Residential Research

The property consultancy anticipates that the housing market may have seen a large proportion of anticipated declines in the last quarter of 2022.

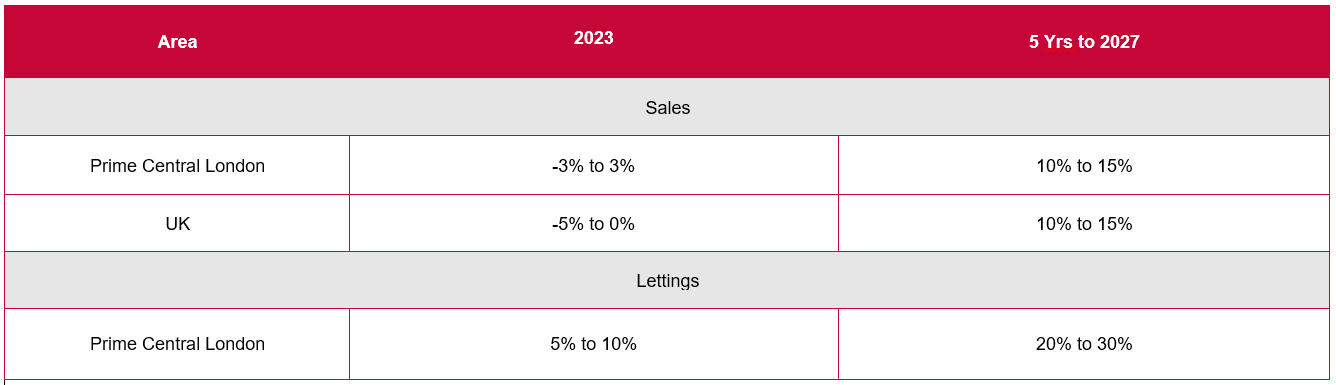

Forecasts for PCL lettings have been revised downwards from the 10 to 15% previously forecast, to growth of between 5 and 10% as a result of affordability constraints and anticipated stock increases.

Matt Henderson, Associate Director Strutt & Parker Research comments, “The start of 2023 has seen more activity than most expected and there are signs that the rest of the year may follow suit. Inflation has peaked, with the Bank of England expecting inflation to fall to between 5 and 6% by the end of 2023. This tenth and latest rise in the base rate is likely to be one of the last increases, and economists expect both the Federal Reserve and Bank of England to likely start reducing rates at the end of this year, or early next.

“The recent rate increase will do very little to affect mortgage rates as lenders have already priced in these rate hikes. As such, we’ll likely witness increased stability and certainty in the market encouraging transactions and stabilising prices.”

For Prime Central London, sales price growth in the year to Q4 2022 was 0.8%, and in line with previous forecasts. However, the last quarter was the second consecutive quarter of negative growth at -0.6%, with prices still almost a fifth down on the 2014 peak. PCL rents grew for a sixth consecutive quarter, with the sharp increase indicated by the proportion of lets agreed at less than £500 per week halving from 38% of total transactions in 2021 to just 19% in 2022. However, with growth of just 0.9% in Q4, a continued high rate of growth is unsustainable.

Louis Harding, Head of London Agency at Strutt & Parker comments, “We’re in a similar position as last year: a scarcity of stock will continue to uphold premiums in the prime London sales market and create disconnect between those markets above £4M and those below. More peripheral and mainstream London markets are likely to not be as robust as those less reliant on borrowing constraints.

“The rental market was well and truly exhausted by autumn last year with the drop off in the last three month’s transactions effectively wiping out gains on the previous quarter. It’s evident that tenants are unable to continue to prop up the rate of climbing rents and, with the sales market a space of uncertainty and frustration, we may see vendors putting their homes into the rental market until stability resumes which will help low stock levels.”

Despite HMRC reporting residential transactions in November 2022 were 13% higher than those for the same period in 2021, and still 1% higher than October 2022, previous forecasts by Strutt & Parker anticipated that high transaction levels were unlikely to be sustained due to increasing economic pressures.

Kate Eales, Head of Regional Agency at Strutt & Parker comments, “The market is one of conflicting messages at present, despite applicant numbers and instruction rates within 10% of those at this point last year, the rise in cost of living, inflation and disrupted mortgage markets means that consumer cautiousness remains high.

“That said, as stability begins to return to the mortgage market, as seen by some reductions in five-year fixed rates and a leaning back into non-variable products, those who are in a position to be able to transact this year will have their confidence bolstered some-what. While some have forecast downturns of up to 10% this year, around half of this negative growth has potentially already been witnessed in the turmoil that followed the mini-budget and resulting mortgage markets.”

Read the full quarterly here.