Although lease lengths have been falling for some years in the UK property market, greater flexibility in office and retail sectors has recently gained significant attention, manifesting itself in a number of different ways. In this blog, we look at recent trends in flexibility, the different types of occupiers that have emerged and at trends set to emerge in the future.

Growing serviced office sector

The number of serviced office centres across the UK has grown considerably. Serviced office take-up totalled 920,000 sq ft in the first half of 2017 with the number of centres, tracked by Instant Offices, growing 11% in 2015/2016. London is ahead of other regional centres in terms of its number of centres. There are 944 serviced office locations in London compared to next highest, Leeds that has under 100 centres.

Volatile business plans

Businesses are increasingly realising that their business plan is likely to change several times over a typical lease term. Therefore, their occupied real estate has to be able to adapt too. For example, we are increasingly seeing occupiers take serviced office space as an overflow solution, or for project work. Having a portion of their business in a serviced office provides vital flexibility, despite disadvantages including the higher costs paid by the tenant during their period of occupation.

Increasing employment in small businesses

According to the Office for National Statistics (ONS), smaller and medium sized companies have been the key drivers of private sector employment growth in the UK. Small and medium sized companies, defined as businesses with between 10 and 249 employees, saw the total number of employees increase by 928,000 over a period from 2010 to 2016. As a comparison, staff at large companies, defined as business with over 250 employees, increased by 761,000 over the same time period.

Smaller companies will inevitably require more flexible and shorter-let space and are likely to take space with serviced office occupiers, often until the occupier feels sufficiently established to take a traditional lease. A number of landlords are increasingly providing ‘incubator’ space, a serviced office solution whereby less-established occupiers can take space in the incubator before taking space on another floor in the building.

Strong demand for shorter leases and break options

Where companies opt for traditional space, research has shown a reduction in both lease length and period of time between breaks. According to the UK Lease Events Review 2016, leases of 10 years and shorter accounted for 76.5% of new lets in the first half of 2016, an increase from 70.7% in 2015 on a rent weighted basis. In the Central London office market, average rent-weighted lease length has declined from 11.5 years in 2011 to 7.3 years in 2016.

During the first half of 2016, 38% of leases signed included a break option, rising from 35.4% in 2015 and 37% in 2014. This suggests tenants are no longer so willing to sign a lease without first ensuring a degree of flexibility.

Fall in office unit size

Finally, the average size of unit that occupiers require has also fallen, a trend that can be attributed to a business’s desire to use their space more efficiently. A recent example of this is PwC which recently announced it would be consolidating its London staff into two offices, removing the need for its 150,000 sq ft office at Hays Galleria. PwC’s investment in technology, allowing staff to work flexibly, has allowed this shrinkage in occupation.

International Lease Accounting Standards

The introduction of the new International Accounting Standard for IFRS leases will drive occupiers to take more flexible leases. The standard means that occupiers will be required to list rent on the balance sheet as a liability and an asset, reflecting the tenant’s right to use, where before rent was able to be recognised as an expense. The new standard will require companies with large lease commitments to evaluate their situations. It is expected that this will lead to an increase in the number of companies seeking shorter lease commitments, or taking space in serviced offices. The new IFRS lease standard covers leases with minimum terms of 12 months or more, it does not apply to licences.

Other forms of flexibility

In order to be flexible in existing leases, tenants are able to sublet or assign existing space – websites such as Spacegrab or Liquidspace facilitate this process by allowing businesses to sublease space without spending time and resources. This, in turn, allows new tenants to take the space on a sublease or assignment on a short-term basis, such tenant-offered space is often fitted out allowing tenants to move in more quickly.

Flexible retail has a key role in placemaking

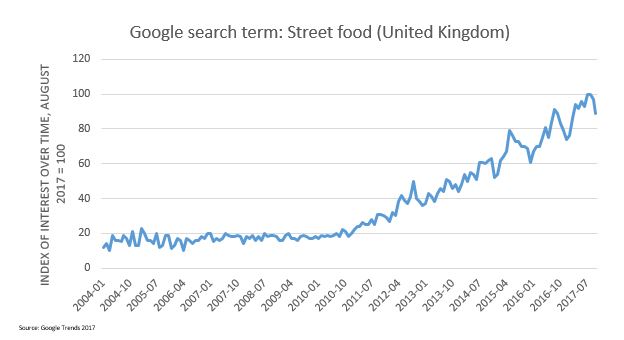

Landlords are also able to turn office districts into mixed use destinations by providing a flexible food offering. In Canary Wharf for example, street food is playing an increasingly key part of operations by contributing to the area’s placemaking. A growth in mobile payment solutions has allowed tenants to operate in more flexible scenarios where a tenant is no longer restricted by its environment and thus street food is expected to benefit considerably. The graph below demonstrates the increasing Google search interest of ‘Street food’ in the UK.

In the retail real estate sector, serviced offices and flexible working are not applicable. However, leases have shortened to the same extent as with office leases, suggesting other factors are at play affecting retail occupiers’ demand for more flexible space.

In prime markets, landlords have not had to make flexible lease adjustments to a significant extent, as demand is still high for such units and occupiers crave certainty of occupation. However, such markets are not immune from structural change, primarily the rise in online retail. Large shopping centres for example have increasingly made use of pop-up retail in order to regularly keep their retailer offering up-to-date. This acts in a similar way to incubator space by enabling up-and-coming retailers to lease space in prime locations, also contributing to the shopping centre’s overall vibrancy.

The impact of technology

Finally, a growth in new technologies helps to remove any ‘sunk costs’ that may have previously prevented tenants from pursing greater flexibility. For example, new technology has enabled a reduction in the cost of moving in and out of a property. The removal or reduction in such costs will allow tenants to hold more flexible leases, and is also likely to make tenants less likely to renew at the end of their lease. Primarily, the growth in laptops, tablets, mobiles and cloud networks can reduce moving costs, enabling tenants to move to more flexible models of leasing.

Find out more about our Property Futures research here.