Matthew Henderson

Associate Director, Residential Research

Associate Director, Residential Research

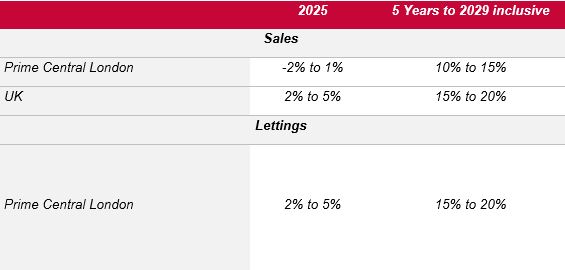

Strutt & Parker anticipates that the housing market will see a continuation of the boost in transactions that has carried on through the latter half of 2024 into 2025. Q1 saw more than 338,000 transactions for the first time since 2022. The upward pressure on values that has been caused by this will remain throughout the year. This has been driven by the mainstream markets with more prime markets not fairing as well, prime London an example of this as global uncertainties and changes to the non-dom status hang over the market.

“Uncertainty – especially at higher price points – is one of the greatest dampeners of the housing market. This causes buyers to sit on their hands and take stock rather than look to transact. American policy and the rise in global conflicts lead to further uncertainty and decrease the risk appetite of many investors” comments Matt Henderson, Associate Director in Research at Strutt & Parker.

Prime Central London transactions stayed flat in the sub-£1m, up 12% against the same quarter last year. However, at the £1m+ price points the market has struggled with transactions falling due to global uncertainties. Much of these falls can be attributed to the ending of the non-domiciled status which have impacted sales over the last year since the Conservatives first announced that changes would be made. Agents are hopeful that the rate cuts will drive further market activity in the mainstream market that will start to influence higher price points.

James Gow, Head of London Agency at Strutt & Parker adds “Q1 sales transactions were similar to 2024, although the availability of properties on the market was notably lower. The market can be seasonal, and we typically find that spring and summer to be buoyant. We have seen a healthy increase of instructions, and both buyer enquiries and registrations are at encouraging levels. Our recent sales confirm that best-in-class property creates competitive bidding and strong results. Looking ahead, we expected the market to continue its upward trajectory, driven by lower mortgage rates, economic stabilisation, and sustained demand for luxury properties.”

Rents in Prime Central London grew by 0.7% in Q1 2025. This is a return of PCL rental values as new let figures for this quarter show a slow market; strong compared to a very weak Q4 last year, yet 37% down on Q1 2024. The market in PCL remains dominated by flats making up 92% of new lets, with turnkey family homes the most under supplied.

Agents have reported that the upcoming Renters’ Right Bill has made the market unviable for a growing number of landlords who have been taking this opportunity to enter a more active sales market worsening an already problematic supply-demand imbalance.

Matt Henderson concludes, “the instability of other markets, and geographies may make the security of prime bricks and mortar in the UK come to the fore. The UK, and more so London, has a ‘safe haven’ status. The security of Prime real estate may attract investors who are looking to move funds away from areas of global conflict and less stable environments. In addition to the reducing cost of mortgage we are prudent yet optimistic for the remainder of the year.”

Read full report here.