Matthew Henderson

Associate Director, Residential Research

Associate Director, Residential Research

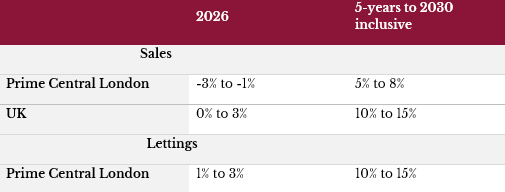

Strutt & Parker has a positive view for the UK housing market with growth of up for 15% over the next 5 years. Transaction levels in first three months of this year reached 270,000. Although this is below the 300,000 mark that the previous six quarters, and the pre-covid years averaged, this is typically the quarter that experiences the lowest transactions.

However, this is a bifurcated market; more affordable, more northerly regions have achieved over 3% growth over the 12 months to February 2026. The less affordable regions – those with the highest house-price-to-earnings ratio – have typically seen a fall in value over this period.

Made up of the local authorities with the highest house-price-to-earnings ratio, the PCL market has seen negative price growth over the start of 2026. Completed deals over £1m fell by around a third this quarter. However, this is largely due to cyber-attacks on the council websites of the Royal Borough of Kensington and Chelsea (RBKC) and the City of Westminster which have dramatically extended conveyancing times.

Sales agreed show a much more positive story, 14% up on the final quarter of last year, and 2% below Q1 2025. The times to complete these sales are likely to be longer, agents have reported having to receive plans and surveys on paper during Q1. The technical issues created by the cyberattack look to be resolved, however there is still a significant backlog that needs to be worked through. Longer completion periods will inevitably lead to a higher proportion of fall throughs, but the volume of agreed sales paints a positive picture.

“The PCL market has certainly had to readjust to changes in taxation impacting the international market that works very uniquely in Prime London. However, this has created a huge opportunity for UK based buyers, particularly families, to upgrade and upsize their real estate both in terms of family homes and portfolios.” says Claire Reynolds, Strutt & Parker’s National Head of Sales.

Claire continues “Central to buyer motivation at present is long term investment and wealth preservation, with London continually cited as an important base on a global stage for international families thanks to the education and culture on offer. Looking forward, pricing and presentation will be key in a highly sensitive market that champions turn-key best in class homes, while on a global stage we anticipate a positive shift in Middle Eastern enquiries seeking stability and security, while US markets are likely to base themselves on investments with a currency advantage and long-term hold, rather than short term play.”

Anna Ambrose, National Head of Lettings, comments “The lettings market has seen what we would call a ‘traditional Q1’, both in PCL and regionally. Moderate rental increases have continued and new lets have maintained a steady rate, although there are signs the summer uptick is coming early. Tenants across the board are looking for outside space of their own, or at the least being situated within a good proximity of a local park.

“The super-prime end of the London market has been far more active, experiencing multiple times the number of lets we saw in Q1 last year. This has come with a shift in the profile of these tenants. Many domestic potential buyers, particularly around Kensington, have decided that they would rather let than buy in the medium term.

“The cost of stamp duty is often the same as two-to-three years’ rent and with the sales market not promising capital growth, letting at this end of the market looks like a more fiscally rational decision. As has become the norm, best-in-class homes are achieving premium rents and seeing the most competition. These are often properties that have been fitted out for ownership.”

Rents in PCL have increased by 0.5% over the final quarter before the Renters’ Right Act came into force on 1st May. As is typical in this very seasonal market the number of lets in Q1 was closely aligned with Q4, down 3%, yet new lets were 25% up on a weak Q1 last year. Volumes have returned to a more traditional post-covid level with around 1,500 new lets each quarter, with a strong 2,000+ Q3.

Matt Henderson, Residential Research Lead adds “We are currently in an economic and geo-political period that makes forward-looking in most markets, and acutely in residential markets, even more challenging and hypothetical than it always has been. International conflicts have an increasing impact; rippling through our ever more globalised and interwoven world.

“The human impact of the Iran War, and its disruption to the Gulf, will no doubt see wealth look to settle elsewhere in the longer-term. However, ascertaining when these decisions are made, or measuring the arrival of wealth to the UK, is more difficult.

“In the more immediate future, the impacts of a higher cost debt market will weigh on housing transactions. Political instability is not helping, with the uncertainty pushing up gilts.

“Regardless of this we are still seeing determined buyers looking to move across the country; some driven by personal motivations, and others sensing an opportunity for value. The PCL rental market has settled back into its steady seasonal nature, regardless of all the commentary surrounding the Renters’ Rights Act.”

Read full report here.